Comprehensive Guide to Personal Loans

This guide delves into the intricacies of personal loan options across several English-speaking countries, providing detailed insights into loan terms, interest rates, and application processes. In doing so, it explores the landscape of unsecured and secured loans, highlighting the vital role they play in financing personal endeavors or consolidating existing debt.

Understanding Personal Loan Options

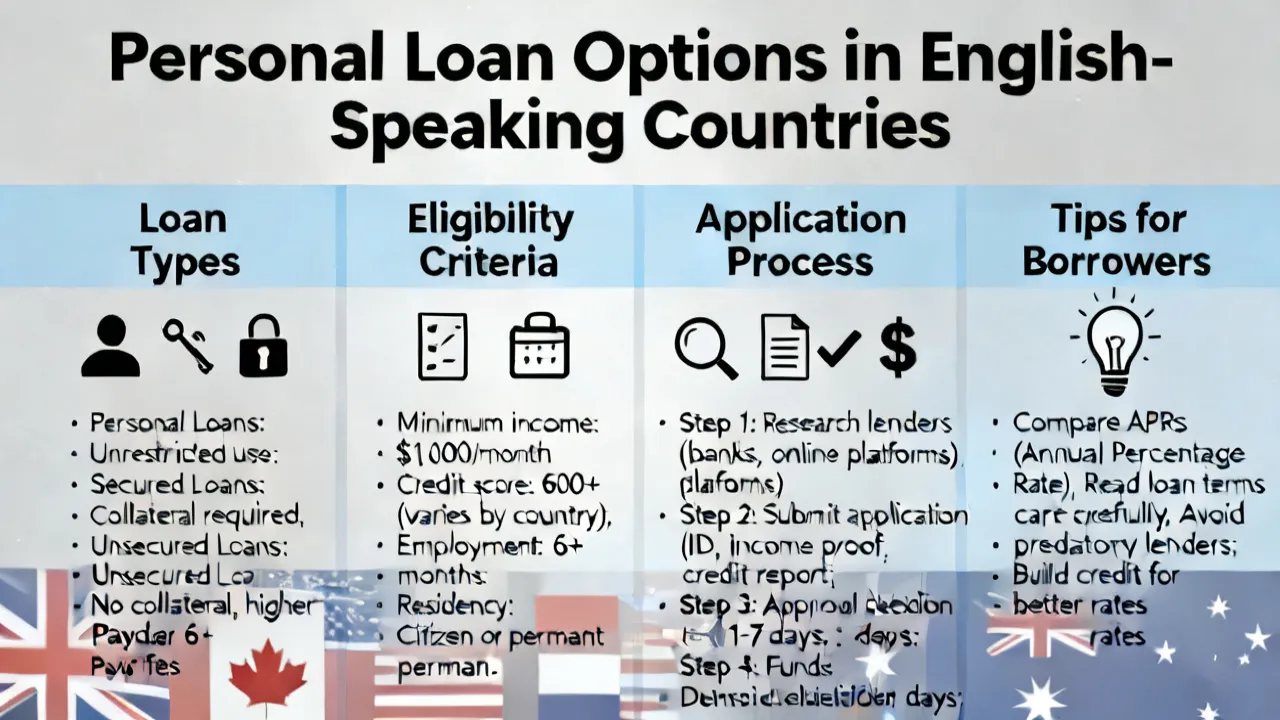

The landscape of personal loans is diverse, catering to various financial needs, from education and medical expenses to debt consolidation and emergency funds. This guide explores the personal loan options available in prominent English-speaking countries, helping prospective borrowers navigate the often complex world of financial services. With a thorough understanding of the various products available in different markets, you can make informed decisions that align with your financial goals. Personal loans can vary significantly based on economic conditions, lending regulations, and consumer needs, making it necessary for one to fully comprehend the elements involved in obtaining and managing these loans.

Personal Loans in Australia

Australia offers an array of personal loan options, catering to both secured and unsecured needs. Leading industry players include Harmoney and ANZ Bank, each providing distinct features and services aimed at different consumer profiles.

| Provider | Loan Amount | Interest Rate | Fees | Repayment Terms |

|---|---|---|---|---|

| Harmoney | AUD 2,000–70,000 | From 5.76% p.a. | Establishment fee: AUD 275 or 575 | 3, 5, or 7 years |

| ANZ Bank | AUD 5,000–75,000 | From 6.99% p.a. | AUD 150 establishment fee | 1–7 years |

The Australian loan market is known for its competitive rates and flexible terms, making it easier for consumers to find products that meet their specific needs. Online lenders like Harmoney have revolutionized the lending landscape by allowing peer-to-peer lending, making funds accessible to borrowers while providing investors with profitable opportunities. Traditional banks such as ANZ maintain their appeal with their established reputation and comprehensive service offerings, which often include loans tailored for purposes like car purchases or personal emergencies.

For individuals considering a personal loan in Australia, it’s essential to compare different types of loans - both secured and unsecured - to understand the implications of each. Secured loans, which are backed by collateral, generally come with lower interest rates but carry the risk of losing the asset if repayments cannot be met. Unsecured loans offer higher flexibility but usually at the cost of higher interest rates and a stricter approval process. Overall, evaluating your financial standing and understanding how personal loans fit within your broader financial strategy is vital before making any decisions.

Exploring Loan Options in Canada

Canadian residents have consumer-friendly personal loan options, prominently from TD Bank and RBC. The personal lending landscape in Canada is shaped by a mix of traditional banking institutions and new fintech companies, creating a versatile borrowing environment.

| Provider | Loan Amount | Interest Rate | Fees | Repayment Terms |

|---|---|---|---|---|

| TD Bank | CAD 5,000–50,000 | Starting at 8.99% p.a. | Varies by province | 1–5 years |

| RBC | CAD 5,000+ | From 7.99% p.a. | Relevant administration fees | Up to 5 years |

In Canada, the loan application process often includes a thorough assessment of credit scores, income verification, and employment status. This due diligence is standard to minimize risks for lenders while ensuring borrowers can fulfill their financial obligations. Furthermore, Canadian lenders often provide various repayment options and opportunities to renegotiate terms if financial circumstances change.

Canadians seeking personal loans should take advantage of resources like online calculators to simulate loan scenarios based on differing amounts, terms, and rates. Doing so helps visualize the total cost of borrowing, including interest and associated fees, allowing for more informed financial planning. Factors such as one's credit profile and income level inherently impact the type of loan and interest rates offered, highlighting the importance of maintaining good credit health prior to seeking a loan.

Navigating UK Personal Loan Options

The UK offers competitive personal loans, notably from Lloyds Bank and Santander UK, each designed to meet distinct financial needs. The personal loan market is characterized by a mix of high street banks and online lenders, providing consumers with numerous planning and borrowing avenues.

| Provider | Loan Amount | Interest Rate | Fees | Repayment Terms |

|---|---|---|---|---|

| Lloyds Bank | £1,000–50,000 | Starting at 4.9% p.a. | No application fees | 1–7 years |

| Santander UK | £1,000–25,000 | Starting at 5.5% p.a. | No fees for repayment | 1–5 years |

Source: Lloyds Bank, Santander UK

The flexibility offered by UK lenders often includes options for early repayment without incurring penalties, making it easier to manage outstanding debts. The competitive interest rates available for borrowers, especially for those with strong credit histories, create an appealing incentive for seeking personal loans to consolidate higher-interest debts or fund significant purchases. Coupled with no application fees from leading banks, borrowers can save additional costs while securing the financing they need.

For consumers in the UK, it's vital to thoroughly compare offers from different lenders, putting emphasis on the annual percentage rate (APR), which encompasses the costs of borrowing inclusive of fees, and not just the interest rate itself. The APR allows for a clearer insight into the true expense of taking a loan, making it easier for individuals to seek the most cost-efficient option tailored to their financial circumstances.

Understanding the US Personal Loan Market

In the United States, businesses such as Wells Fargo and SoFi dominate the personal loan arena, leveraging technology and traditional services to meet consumer demands. American borrowers have a vast array of choices, with diverse lending practices spanning from traditional banking institutions to innovative online fintech companies.

| Provider | Loan Amount | Interest Rate | Fees | Repayment Terms |

|---|---|---|---|---|

| Wells Fargo | USD 3,000–100,000 | 7.49%–23.74% p.a. | Late payment fees apply | 12–84 months |

| SoFi | USD 5,000–100,000 | 6.99%–21.99% p.a. | No origination or late fees | 2–7 years |

Source: Wells Fargo, SoFi

American consumers benefit from a highly competitive lending environment, often allowing them to secure loans with favorable terms. The presence of peer-to-peer lending platforms and online lenders has significantly changed the funding landscape, encouraging traditional banks to offer more attractive rates and flexible repayment terms. As such, borrowers now have the opportunity to tailor loans to specific needs, whether for personal use, home improvement, or debt consolidation.

For borrowers in the U.S., it is crucial to understand the factors impacting credit scores, as these directly influence the loan rates one may qualify for. Regularly monitoring credit reports and exercising responsible financial management can greatly reduce borrowing costs over time. Additionally, many lenders offer educational resources to help borrowers understand the implications of personal loans, with tools available to assist in budgeting and planning repayment strategies that align with one's financial goals.

Steps to Apply for a Personal Loan

Applying for a personal loan typically involves several key steps:

- Evaluate your financial situation and determine the required loan amount. Assess your existing debts, income, expenses, and the specific purpose of the loan to calculate how much you can realistically afford to borrow.

- Research and compare loan offers from various banks or financial institutions. Make use of online comparison tools to view interest rates and terms from multiple lenders, tailoring your search based on your credit profile and financial needs.

- Check your credit score, as this will impact the terms and rates offered. Understand the factors that contribute to your score, and consider taking steps to improve it before applying.

- Gather necessary documentation such as identification, proof of income, and credit history. Lenders often require specific documents for verification, including tax returns, pay stubs, or bank statements, to evaluate your application.

- Submit an online or in-person application and await approval. Depending on the lender, approvals may be instant, while others may take several days to process.

- Once approved, review the terms and conditions before accepting the loan. Pay special attention to the APR, repayment schedule, and any associated fees that will affect your total cost of borrowing.

- Plan a repayment strategy to ensure timely payments. Create a budget that incorporates the loan repayments into your financial planning, and consider setting up automatic payments to avoid late fees and maintain good standing with your lender.

Each step is crucial in ensuring that your experience with personal loans is positive, allowing you to avoid potential pitfalls while enhancing your financial literacy. Recognizing the importance of your credit profile before entering the loan market will empower you to negotiate better terms and secure funds that best fit your needs.

FAQs

- What is the difference between secured and unsecured loans? Secured loans require collateral, such as a car or home, whereas unsecured loans do not, often resulting in higher interest rates for unsecured options as lenders take on more risk.

- What credit score is needed for a personal loan? A good credit score (700+) generally secures better rates and terms, although specific requirements vary by lender, with some offering loans to individuals with lower scores at higher rates.

- Can I repay the loan early? Some lenders allow early repayment without penalties, though it's essential to verify the terms; doing so could save on interest payments if you have the means to pay off the loan sooner.

- How long does it take to get approved for a personal loan? Approval time can vary, ranging from minutes with some online lenders to a few days with traditional banks; it's advisable to provide complete and accurate documentation to avoid delays.

- What can I use a personal loan for? Personal loans can be used for a variety of purposes, including consolidation of debt, home improvements, major purchases, medical expenses, or funding education; however, reviewing lender policies on acceptable uses will help clarify your options.

Disclaimer

1) The above information is based on online resources, valid as of October 2023. 2) Specific loan requirements and repayment terms are subject to official regulations, which may vary by institution and should be confirmed directly with lenders. 3) This guide will not be updated in real time, so it's advisable to check for the most current information during your research.

References

All sources are based on provided URLs for the respective banks and financial institutions. Understanding the nuances of personal loans is critical to ensuring financial well-being and achieving long-term goals. By engaging in thorough research and maintaining a clear awareness of your financial landscape, you can better navigate the intricacies of borrowing and repayment.

Final Thoughts

As you consider personal loan options, remember that every individual’s financial journey is unique. Customizing your approach based on your specific needs, preferences, and financial situation is essential for successful borrowing. Whether you're managing existing debts, making a significant purchase, or financing an education, taking the time to research and fully understand your options is the key to maximizing the benefits of personal loans while minimizing costs.

Additionally, consider seeking professional financial advice if you're uncertain about any aspect of borrowing. Financial advisors can provide insights tailored to your personal circumstances, helping you determine the best strategies for debt management, investment planning, and securing the right personal loan for your needs.

Ultimately, personal loans can be a powerful financial tool when used thoughtfully and responsibly. Take advantage of the resources available to you and embark on your financial journey with confidence.

-

1

Maximizing Your Purchase: Ram 1500 Deals and Towing Capacity

-

2

Maximizing Benefits of Solar Panels: Costs and Energy Efficiency

-

3

Affordable Stair Lifts for Seniors: A Comprehensive Guide

-

4

The Ultimate Guide to Lab-Grown Diamonds: Ethical & Cost-Effective Choices

-

5

The Ultimate Guide to Weight Loss Injections, Metabolism, and Appetite Suppression